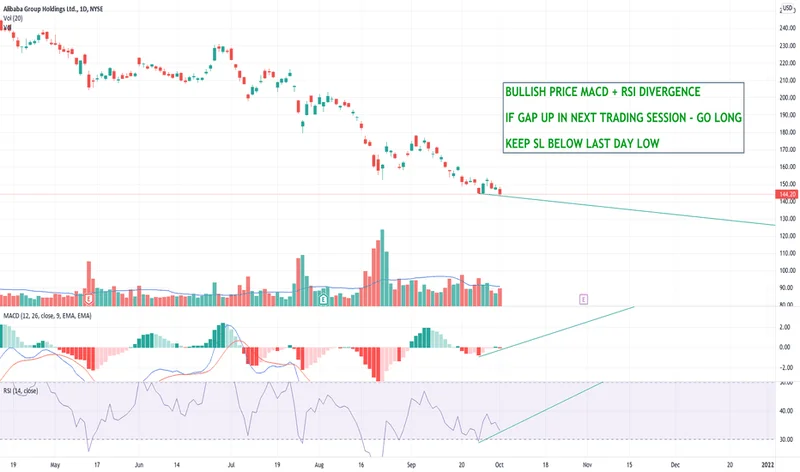

summary:

Alibaba’s stock recently surged, fueled by reports of a stronger-than-expected quarterly r...

summary:

Alibaba’s stock recently surged, fueled by reports of a stronger-than-expected quarterly r... Alibaba’s stock recently surged, fueled by reports of a stronger-than-expected quarterly revenue (we're talking a 5.10% jump to $160.73). The headline? Gains in their AI-powered cloud division. But let's peel back the layers and see if this growth is built on solid ground or clever accounting.

Cloud Gains: Digging into the Numbers

The headline figure everyone's touting is the Cloud Intelligence Group's revenue: 39.8 billion yuan, or $5.59 billion, exceeding forecasts. Adjusted revenue growth supposedly hit 34%. But here's where the analyst's eye needs to focus. Management is quick to mention "restructuring and product adjustments" alongside massive AI and cloud investments. These investments reached roughly 120 billion yuan (that's around $16.8 billion) over the past year. It's like a magician distracting you with one hand while the other is doing the real work. According to Alibaba shares rise as AI drives 34% cloud sales jump, AI is a major driver of this growth.

How much of this "growth" is simply a result of shifting resources and reclassifying existing revenue streams under the "AI Cloud" umbrella? We need to know the like-for-like growth, stripping out these internal adjustments. And while they mention a 15% like-for-like growth excluding Sun Art and Intime, it doesn’t isolate the cloud division itself. It's a classic case of obscuring the true picture with broad strokes. What is the actual organic growth of the AI-cloud sector, removing all the accounting adjustments?

Then there's the profitability question. Non-GAAP EPS missed estimates by $0.20, and RMB EPS plummeted 71%. Management blames product adjustments and heavy investment cycles. But how long can they sustain this level of investment without seeing a more significant return on the bottom line? Cloud margins will be watched closely, analysts say, to gauge whether Alibaba's AI push can deliver sustainable profits. I wonder if this AI push is less about a genuine technological breakthrough and more about investor relations and the need to keep up with the AI arms race.

Retail Revival: A Temporary Boost?

The report also highlights improved retail performance, driven by fast delivery services and a government-backed appliance trade-in policy. One-hour delivery is scaling, which is great. But the trade-in policy is set to expire on December 31st. What happens in early 2026 when that stimulus is gone? Will the underlying demand be strong enough to sustain the current growth rate, or will we see a correction?

Here's where I'd like to see more granular data: What percentage of the recent e-commerce gains can be directly attributed to the trade-in policy versus organic growth? Without that breakdown, it’s impossible to determine the true health of Alibaba's core retail business. I've looked at hundreds of these earnings reports, and this lack of transparency is… concerning.

Furthermore, the report mentions "intense competition in China’s retail market." This is a crucial point often glossed over. While Alibaba is investing heavily in AI, so are its competitors. Are they truly gaining a competitive edge, or are they simply running faster to stay in the same place? And how does this competition impact pricing and margins in the long run?

Alibaba's management likes to draw comparisons to NVDA, suggesting their AI investments will yield similar results. But there's a crucial difference: NVDA is selling shovels in a gold rush. Alibaba is trying to become the gold rush. The risk profile is entirely different.

The market seems to be buying the narrative, with U.S.-listed shares up in early trading. But as someone who’s spent years sifting through financial data, I know that market sentiment can be fickle (especially given the current focus on AI). What matters is the underlying fundamentals, and those are still murky.

Cloud Nine or Cloudy Outlook?

Alibaba's AI cloud story is compelling, but the numbers require a closer look. Are the gains real, or are they the result of accounting maneuvers and temporary boosts? The lack of transparency around key metrics raises serious questions about the sustainability of this growth. Until we see clearer evidence of profitability and organic demand, I’m staying cautiously skeptical.